Eigenlayer Restaking Landscape and LRTs

Eigenlayer’s mission

Eigenlayer restaking was launched in June 2023 on the Ethereum blockchain, allowing users to deposit their LSTs into respective pools. Liquid Staking Tokens are tokens minted by staking protocols in order to represent a stake in a validator, and allows users to use that ETH in other protocols in the form of that minted token while collecting native yield. Restaking is the concept of users pooling their ETH tokens into specific pools in exchange for rewards for securing a crypto economic system. This economic system is used to secure protocols without having to create separate smart contracts using the EVM(the codebase for building apps on Ethereum) for consensus. The validators that participate in this restaking receive a reward in return for securing these protocols. Eigenlayer restaking has attracted 18.6 billion dollars worth of ETH as seen in their TVL (Total Value Locked) due to the rewards of participating in restaking being very profitable.

Source: Defillama

What are LRTs?

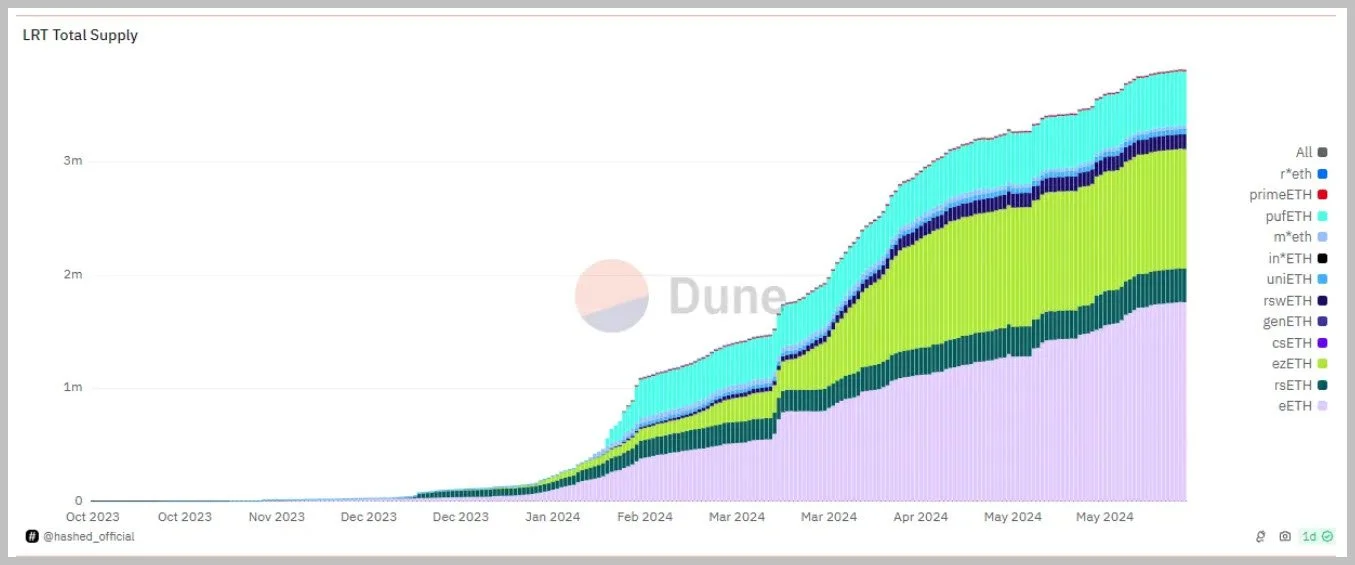

LRTs, which stands for Liquid Restaking Tokens, have made up most of Eigenlayer’s TVL due to the composability nature of the product. LRTs have amassed a whopping 3.82 million ETH, which is worth around 13.5 billion dollars around the time of this article. That’s around 72% of Eigenlayer’s TVL coming from LRTs. LRTs are just like LSTs which I described above, but for Eigenlayer restaking. You stake a certain amount of a LST within a LRT protocol and you get a minted form of the protocol token that represents the ETH you have deposited. This allows you to take part in Eigenlayer restaking and be able to use that ETH in other DeFi protocols making your ETH more capital efficient.

Source: Dune Dashboard made by Hashed_Official

The big incentive for using LRTs is that these protocols are rewarding users with protocol tokens. The top five LRTs seen in the LRT category are Etherfi, Renzo, Puffer Finance, Kelp Dao, and Eigenpie. These protocols have all either released a token already or have announced that they will release a token. The tokens that users get from owning these LRTs and using it in various protocols have been very attractive APYs, leading to this TVL boom.

Source: Dune Dashboard made by Hashed_Official

Pendle’s Role in LRTs

The LRT boom has been largely accelerated due to Pendle. Pendle is a platform that allows users to exchange points gained from using various liquid restaking and staking products in exchange for fixed yield. Pendle utilizes Liquid Staking and Liquid Restaking Tokens to make a market that consists of locking in fixed yield or longing that yield.

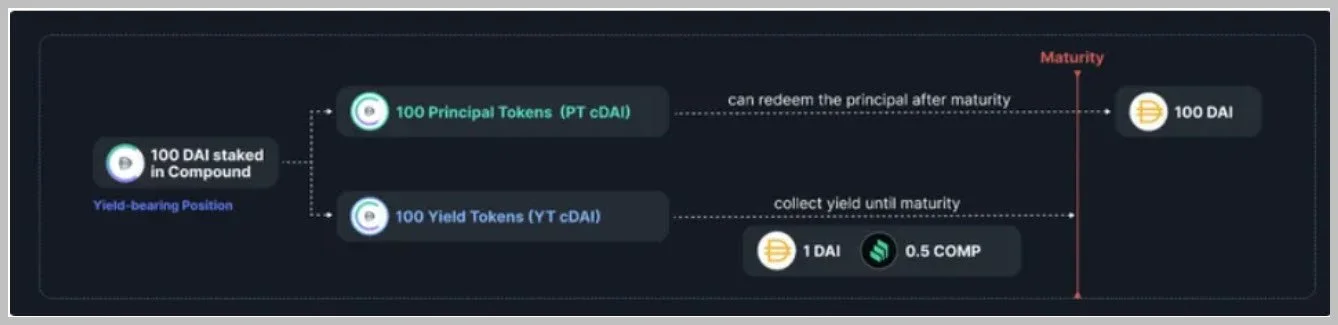

Pendle first takes these yield-bearing tokens and wraps them into two products to make this possible. The two products are PT and YT. PT is the fixed yield product of a yield bearing token, and YT is the way users can leverage/go long yield. The two tokens work in sync with each other using Pendle’s AMM. Suppose users are very bullish on a respective yield bearing token. In that case, they can buy YT to get leverage exposure to those rewards often in the form of protocol points, which are later equivalent to a certain token amount when that respective protocol launches their token. Users are not subject to any locking period when buying PT and YT, and they can be immediately sold into the AMM assuming there is liquidity. This means if the PT price goes up rapidly in a short period of time, the buyers can sell and find a better product with more APY as they have captured most of that yield in that respective farm. It also works the other way around with YTs. Suppose a specific protocol announces an incentive to reward their respective underlying token and get enough people to be more interested. In that case, this will cause the YT value to go up as people want to gain more leveraged exposure to that specific token’s rewards. Of course, a key point about PT and YT is that they are inversely correlated, so it is important to assess the risks before entering any PT or YT.

Source: Pendle Docs; A representation of how the conversion occurs from user deposit to the underlying yield bearing token to PT.

Pendle markets work similar to a zero-coupon bond and the respective coupons. The zero-coupon bond is the PT in which the principal token trades at a discount of its full value, and is redeemable for the full value at a specific maturity date of a pool. This spread between the principal token discount and the full value is what gives the projected APY which is usually high. Meanwhile the YT, is the yield part of the equation in which users go long yield in many multiplies and earn yield on their leveraged exposure to the underlying token rewards until maturity in which their initial capital goes to 0, while the rewards are the proceeds they receive.

Source: Pendle Docs; Representation on how PT and YT pools work until maturity

For example, let’s say the Etherfi ETH market has a PT worth 0.95, and therefore, the YT is worth 0.05 as the total of PT and YT is always equal to the underlying asset at a 1:1 ratio. If a user wanted to lock in the PT yield, they would buy the PT at 0.95 and wait until maturity to redeem it for the full value of 1, meaning that they would earn a 5% return on their ETH. On the other hand, if you were bullish on Etherfi ETH’s token rewards, you would leverage your exposure by buying YT. In this case, you would be getting 20x the ETH in Etherfi exposure due to the YT buy of the ratio of 0.05 getting exposure to the yield of the underlying token, leading to the user getting that whole exposure, which equals 1 as described above and so they get 20x the exposure for the risk they take.

Due to this phenomenon, people have been trading these attractive APYs for these underlying yield tokens a lot, from locking in a lot of APYs for their ETH using PTs to fully betting on the token rewards being very lucrative by aping YTs. It has happened mostly in LRTs as most of these protocols have either recently launched their token or are planning to launch their token, keeping the attention economy of users.

Future of Restaking

Eigenlayer is now incorporating their recent token launch, $EIGEN, into their cryptoeconomic security model by letting users stake their Eigen to the same validators/protocols as their LSTs in order to achieve decentralization for the EIGEN token. Once they achieve decentralization, the Eigenlayer team plans to make the token tradeable. The risks of Eigenlayer being controlled are key to the future of the protocol and restaking as a model in general.

Vitalik and Sreeram, the founder of Eigenlayer, has pointed out some of the risks of restaking which are:

A faulty bug resulting in Eigenlayer’s protocol getting hacked

Building complex protocols which lead to the security of the ETH blockchain to weaken

Should not rely on Ethereum’s consensus protocol to bail out users of the Eigenlayer protocol if it gets exploited

Recruiting ETH’s consensus for the blockchain for specific applications weakens the core of ETH’s consensus as a whole

Of course, there are risks associated with every protocol, so if Eigenlayer continues to handle their restaking mission well, this will lead to further innovation within Eigenlayer and restaking as a whole. Eigenlayer’s restaking model can set a precedent for other restaking models that come out or are currently live such as Karak Network and Symbiotic if they continue to push innovation as well as be equally careful about the risks.

Thanks for reading!